While the UAE has some of the most advanced and largest spa facilities in the Middle East, other key destinations in the region seem to be picking up on the wellness trend, including Saudi Arabia and Oman, which are beginning to witness a shift in the demand patterns. With greater emphasis on wellbeing and fitness, consumers have been increasingly willing to spend money on wellness, making the sector a fast-growing one. The latest report by Global Wellness Institute issued in October 2018 suggests that the MENA region has more than 6,000 spas, generating nearly US$2.8bn in revenues. The MENA region was the destination for nearly 11 million wellness tourism trips in 2017 with an expenditure worth US$10.7bn generated by inbound and domestic travellers.

In order to have a better understanding about the performance of the hotel spas in the region, Colliers International has assessed data from a sample of 376 treatment rooms across 33 hotels in the UAE, Saudi Arabia and Oman.

UAE Spa Market Performance

Overall Market Performance in 2018

The wellness market in the UAE continues to grow, strongly supporting the overall tourism industry and showcasing the country as a complete leisure destination. However, increasing competition and an influx of price-sensitive travellers have had an impact on the overall revenue generated by spas, especially in Dubai and Abu Dhabi.

Overall, the UAE spa market underperformed in 2018 compared to the previous years. The average treatment rate recorded in the UAE was AED 342, a 4 per cent drop compared to 2017. The capture ratio of hotel guests fell by 3 per cent in Abu Dhabi, while Dubai experienced a staggering decline of 22 per cent in 2018. The treatment rooms utilisation (occupancy) recorded among the UAE spas was 18 per cent in 2018 versus 21 per cent in 2017.

1. Dubai Spa Market Performance

The Dubai spa market has been assessed from a stock of 200 treatment rooms, divided into resort spas and city spas. All of the fourteen KPIs for the overall Dubai spa market showed a negative performance. However, resort spas in Dubai exhibited a better performance than the city spas.

Compared to 2017, Dubai Beach Resort spas experienced a 5 per cent increase in treatment revenue per treatment sold in 2018. However, with an 11 per cent drop in total number of treatments, the total revenue generated among the spas in the sample dropped by 6 per cent.

Meanwhile, the city spas recorded an 8 per cent drop in treatment revenue per treatment sold in 2018 and a 3 per cent drop in the total number of treatments sold. Resort spas continue to outperform city hotel spas, achieving an 18 per cent premium in rate and higher treatment room utilisation (24 per cent vs 15 per cent). Data indicates that consumers find resort spas more appealing, as they have more offerings and services compared to city spas. Moreover, city hotel spas receive a higher share of price-sensitive guests and are more likely to offer discounts to attract guests than spas in the resorts.

Dubai Beach Hotel Spas saw a 1 per cent point decline in the capture ratio among hotel guests, along with an 11 per cent drop in in-house guest ratio, indicating a drop in in-house spa guests among some of the properties in the sample. Increased price sensitivity among the hotel guests, as well as discounts and promotions targeting the walk-ins, can be attributed to the dropping capture rate and in-house guest ratio.

The treatment revenue generated per therapist among the resort spas continues to be higher than the city spas. However, both resort and city spas have witnessed a drop in revenue by 2 per cent and 6 per cent respectively, and a 9 per cent and 6 per cent drop in utilisation of therapist hours, indicating that an overstaffing at spas and an underutilisation of therapists is prevalent in both categories of spas. Spas need to formulate the right marketing and cost-cutting strategies to increase spa revenue as the level of competition increases in the market.

Overall, most indicators for the Dubai City Hotel Spas showed a negative performance except a marginal growth observed in the retail revenue contribution and an overall increase in the in-house guest ratio.

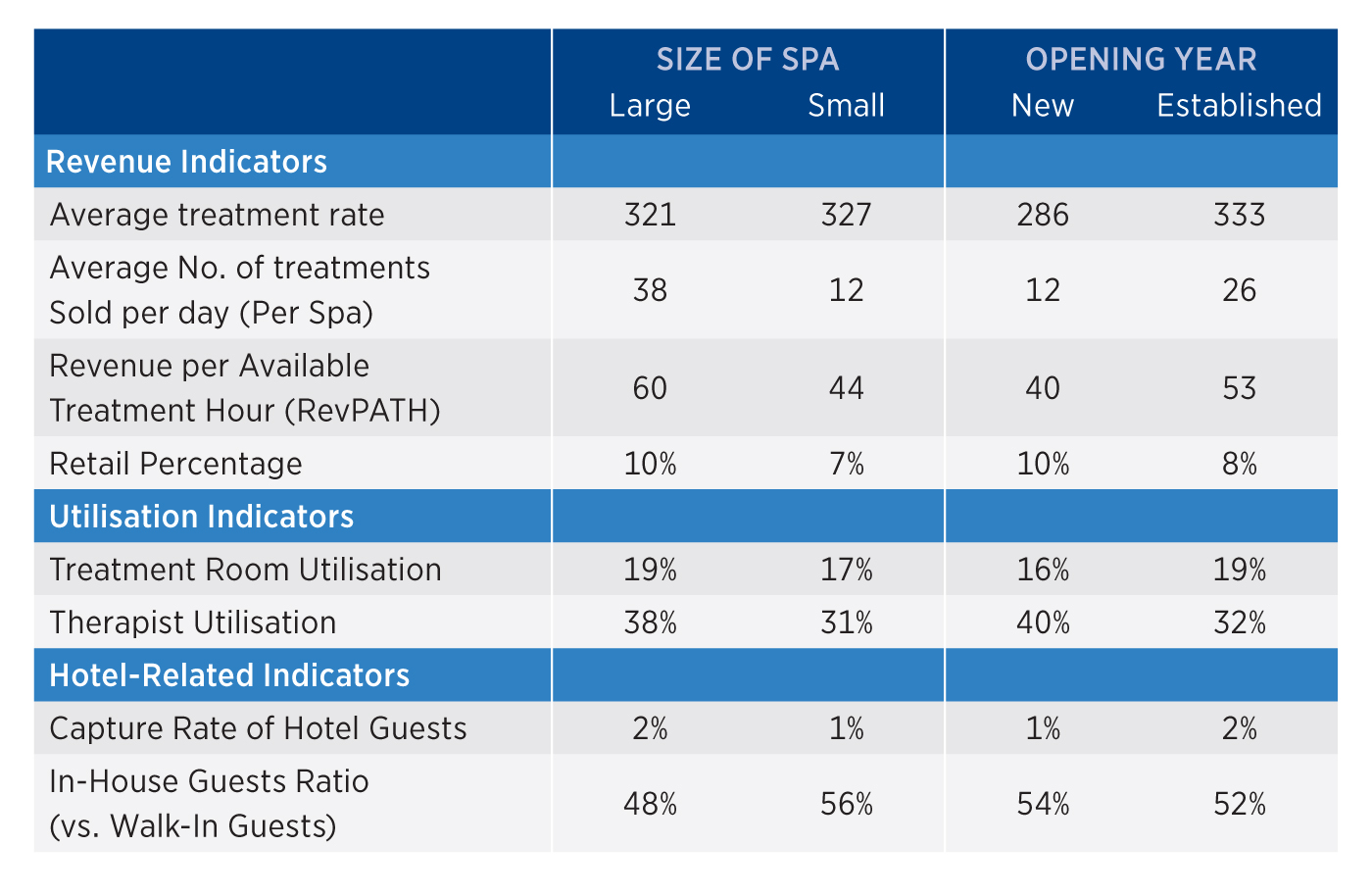

Large Dubai spas in the sample show similar performance to that of resort spas as they benefit from economies of scale. Data also indicate that established spas have outperformed the new spas in all areas except for the in-house guest ratio.

2. Abu Dhabi Spa Market Performance

The Abu Dhabi spa market has been assessed from a stock of 90 treatment rooms, which showed that 2018 was a year of negative performance for the spas in Abu Dhabi. This can be attributed to the shifting source markets and increasing use of promotions and discounts to attract customers. However, the market witnessed a 9 per cent increase in the number of treatments sold, thereby increasing the total revenue generated by 4 per cent despite a 4 per cent decline in the average treatment rate. Revenue per available treatment hour (RevPATH) remained at AED 60.

Treatment revenue generated per therapist and therapist utilisation have seen a decline in 2018 compared to previous years, indicating the underutilisation of therapists and the possibility of an increase in the number of therapists among the spas.

The spas in Abu Dhabi enjoy a higher percentage of walk-in guests compared to in-house guests (64 per cent), thereby depending lesser on tourists and travellers to generate revenue. It is also interesting to note that Abu Dhabi spas have higher capture rate of hotel guests (3 per cent) than Dubai spas (1 per cent) do.

Saudi Arabia Spa Market Performance

The Saudi Arabian wellness industry is evolving. With a young demographic base and a trend towards a mindful approach to wellness, the wellness industry in the country is more geared towards consumers who want to adopt healthier lifestyles. This is evidenced by the recent emergence of spa and fitness centres targeting both men and women. Saudi Arabia’s cultural and social landscape also make wellness centres ideal locations for networking and socialising, particularly for women. The performance of Saudi spas has improved over the last three years, with all the revenue indicators showing positive change compared to previous years, including the average treatment rate, which increased by 16 per cent in 2018. Revenue generated by the spas in general has increased, despite a 22 per cent drop in the average number of treatments sold per day.

Saudi Arabian spas enjoy relatively higher capture rate of hotel guests (7 per cent) compared to other markets in the region. A higher percentage of walk-in guests (82 per cent) indicate the growing demand for spas in the domestic market. Treatment room utilisation and therapist hours saw a drop in 2018 by 7 per cent and 2 per cent respectively, indicating that Saudi Arabian spas need to improve upon these KPIs in order to maximise the revenues and leverage the fact that Saudi Arabia has a limited number of luxury spas.

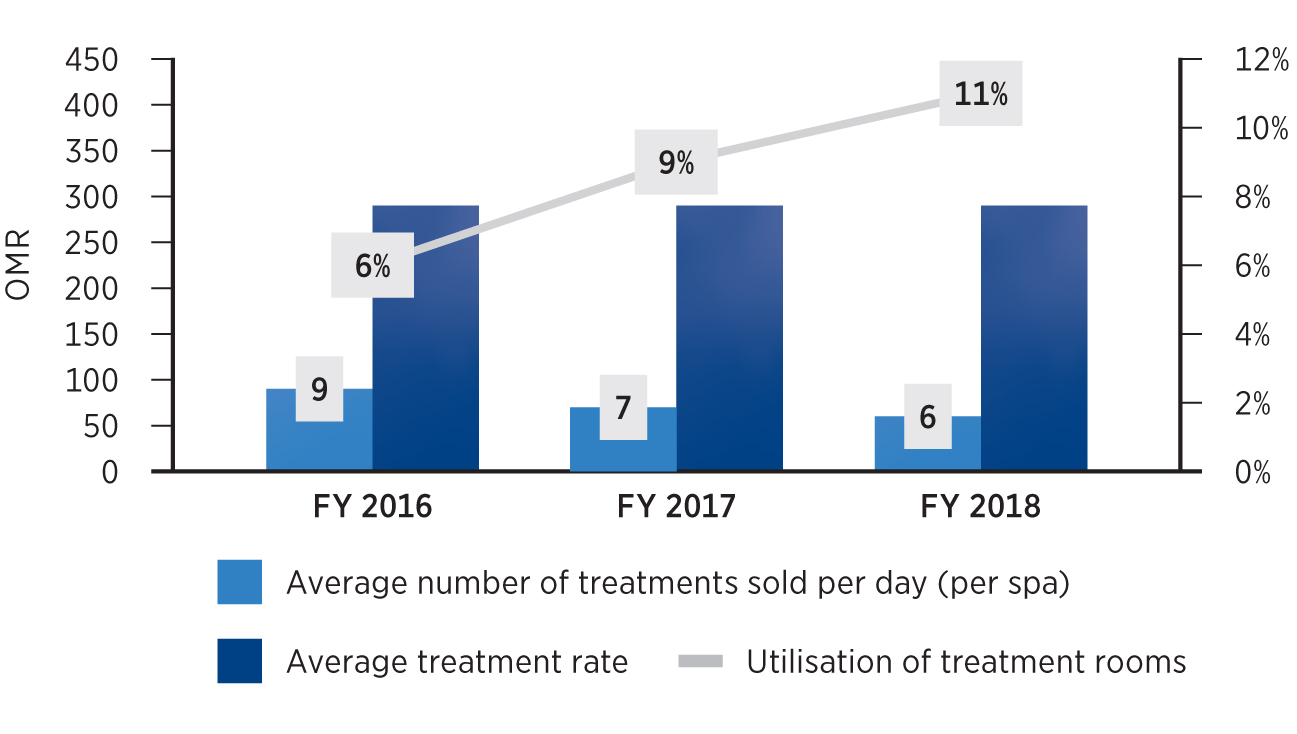

Oman Spa Market Performance

Oman has grown as a leisure destination in recent years. The evolving wellness tourism market is expected to promote Oman’s profile as a holistic leisure destination in the coming years.

The performance by the spas in the country has been commendable and has experienced considerable improvement compared to last year’s performance. The revenue per available treatment room increased by 35 per cent to reach OMR 53 in 2018, while revenue per treatment sold also increased, by 2 per cent, to reach OMR 40.

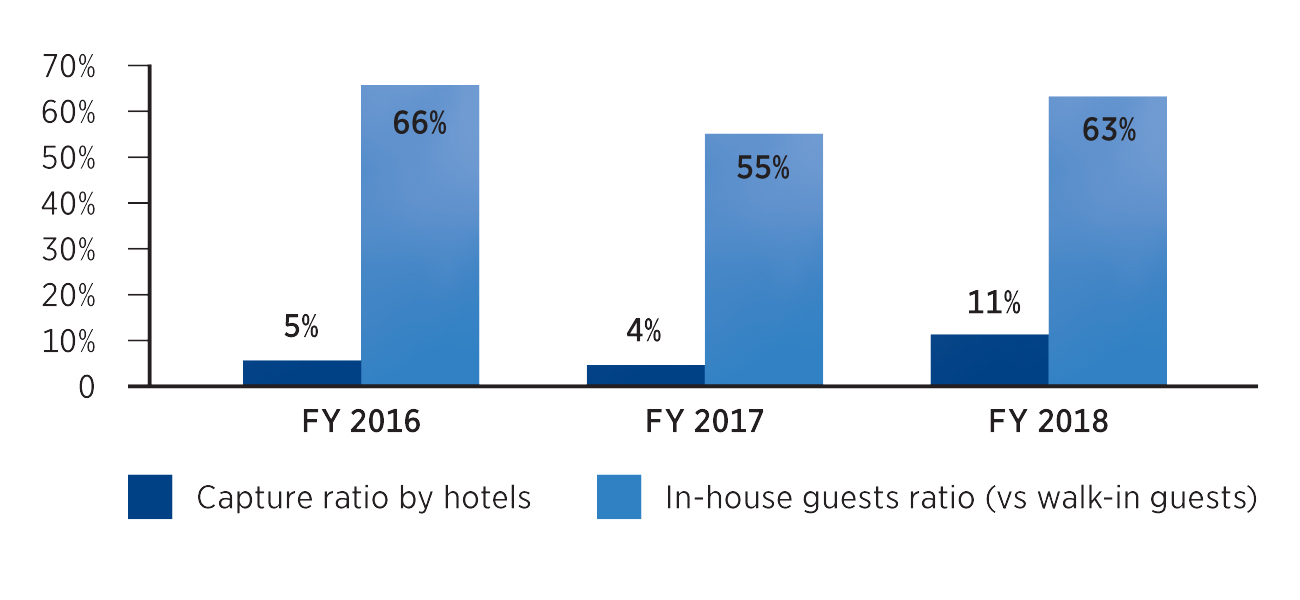

An 11 per cent capture rate of hotel guests indicates the immense potential for wellness in Oman, especially among the luxury hotel segment. The figures also show that the in-house guest ratio has seen an improvement to 63 per cent in 2018, compared to 55 per cent in 2017. The improvements in the aforementioned metrics indicate the growing willingness among the leisure guests visiting Oman to indulge in wellness programmes.

Treatment revenue generated per therapist and therapist utilisation have seen an improvement in 2018 compared to previous years, indicating the better utilisation of therapists in the spas. Although the treatment room utilisation (11 per cent) is relatively low compared to other regional markets, spas are increasingly becoming more efficient, which is evident in the improving ratios observed in 2018. This trend is expected to continue in the coming years, with an increased focus on spa and wellness components by upcoming hospitality developments in Oman.

Outlook

The outlook of the spa and wellness industry in the region looks highly optimistic and robust. The growing global wellness market has also significantly influenced the progress of the regional wellness industry. Increased investor interest is visible throughout the region.

‘Wellness’ has become one of the keys components/concepts for many newly launched megaprojects; a few examples include Amaala, a luxury destination project recently launched in Saudi Arabia, which focuses on wellness tourism, while other mega projects such as The Red Sea project and NEOM will also cover wellness as one of their key components. The emergence of dedicated wellness centres in the region, such as the MAG Creek Wellbeing Resort in Dubai or the eco-friendly Al Zorah Development, is another key growth area for the industry.