|

|

Health Club Management Handbook - World of fitness

Industry insights

|

|

| World of fitness

|

Kristen Walsh analyses the key findings from the recent 2017 IHRSA Global Report

|

HEADLINE NUMBERS – 2017 IHRSA GLOBAL REPORT

|

|

|

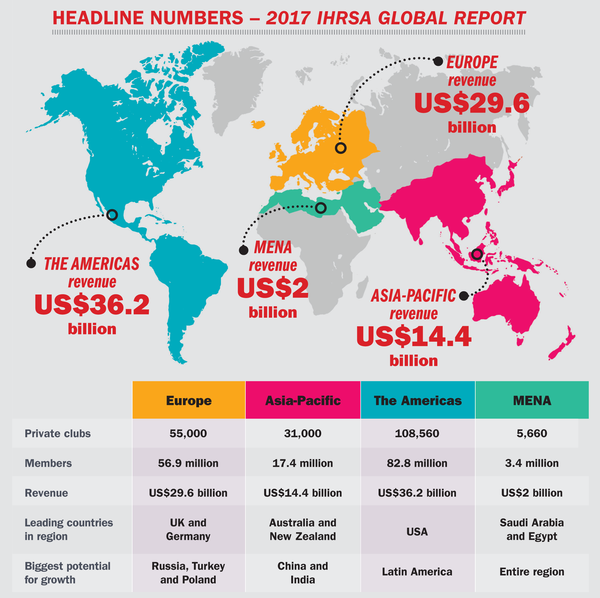

The private sector of the global health and fitness club industry is on a high, with continued growth in 2016, according to the 2017 IHRSA Global Report. Total industry revenue reached an estimated US$83.1bn, as approximately 200,000 clubs served 162 million members worldwide. The markets in North America and Europe continued to grow, while health club markets in Latin America also posted strong performances (see HCM June 2017, page 70). The outlook for the private health club industry is promising and is expected to thrive in the global marketplace, serving consumers with a variety of health and fitness needs. With access to a profusion of fitness amenities, instructors and personal trainers, club operators are well positioned to lead us into a healthy future.

|

|

|

|

Europe

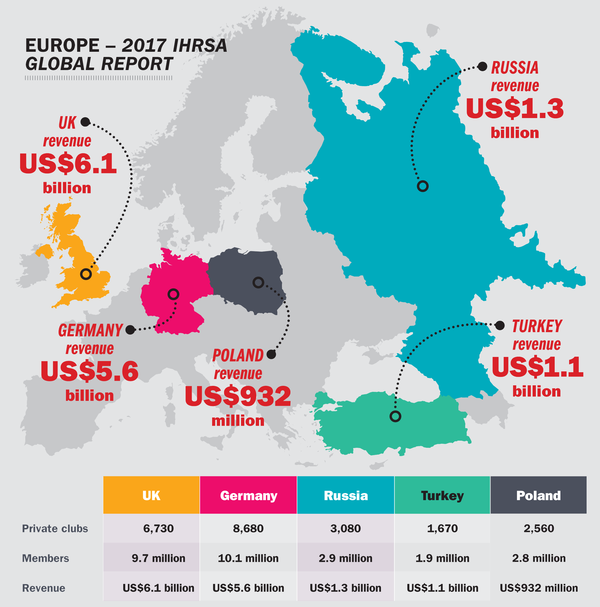

In spite of a weakening euro and challenges in the political landscape, the fitness sector in Europe continued to be robust. The European health club market serves almost 57 million members, with around 55,000 health and fitness clubs generating more than US$29.6bn revenue.

The UK and Germany continue to lead all markets in Europe. In the UK, based on research by LeisureDB, 9.7 million people belong to a private corporate health club, up from 9.3 million a year ago. Approximately 6,730 facilities in the UK generate a collective US$6.1bn in industry revenue. Germany attracts more than 10 million members to 8,680 facilities and generates US$5.6bn in revenue.

According to the 2017 European Health & Fitness Market Report – by Deloitte in partnership with EuropeActive – Europe has strong prospects for growth, not only in the mature markets of Western Europe, but also in Eastern Europe. Especially in Russia, Turkey and Poland where penetration rates are among the lowest in Europe, signifying real growth potential.

| |

|

McFit is currently the largest fitness centre chain in Europe |

| |

|

| EUROPE – 2017 IHRSA GLOBAL REPORT |

| |

|

|

|

Middle East & North Africa

Based on findings gathered by The FACTS Academy – industry experts based in Egypt – approximately 3.4 million members utilise 5,660 private health clubs in 10 markets in the Middle East and North Africa (MENA). These 10 markets collectively generate around US$2bn in industry revenue. Saudi Arabia leads all markets in this region in terms of revenue with nearly US$620m generated at 1,100 health clubs, collectively attracting 817,500 members. However, in terms of club count and memberships, Egypt leads all MENA markets with 1,680 facilities and 957,500 members.

Despite conflicts in several MENA countries, there remains a demand for fitness facilities as consumers seek to exercise and reap the benefits of an active lifestyle. Successful international fitness operators, including Fitness First, Gold’s Gym and World’s Gym, have expanded into the Middle East.

In less than a decade, Fitness Time, based in Saudi Arabia, grew to more than 100 club sites, highlighting the huge opportunities in the MENA region.

| |

|

Saudi Arabian brand Fitness Time highlights opportunities in MENA |

|

|

|

THE AMERICAS

North and South American continents

Canada

The IHRSA Canadian Health Club Report indicates that club operators serve nearly six million members at roughly 6,000 facilities in Canada. IBISWorld – an independent global industry market research firm – says revenue in Canada will rise through 2019.

Consumer demand for health and fitness programmes to address obesity concerns, active ageing, proper nutrition and sports performance will help to drive growth.

The USA

In the United States, the levels of health club revenue and membership – as well as the total number of clubs – all rose between 2015 and 2016.

Revenue increased from US$25.8bn in 2015 to US$27.6bn in 2016, while membership improved from 55.1 million to 57.2 million over the same period.

The US private sector club count grew slightly, from 36,180 locations to 36,540 in this time period, according to IHRSA.

Latin America

Leading markets continue to perform well in Latin America. Based on data gathered in the recently updated IHRSA Latin American Report (2nd edn), Brazil is second only to the US among global fitness markets, with 34,510 health clubs. More than nine million Brazilians are members of a health club. In all, 18 markets in Latin America attract nearly 20 million consumers to more than 65,000 health clubs.

| |

|

Equinox has clubs throughout the United States. Could Latin America offer new market potential? |

|

|

|

Asia-Pacific

The health club industry in the Asia-Pacific region served more than 17.4 million members at 31,000 health clubs across 14 markets in 2016 (excluding the Middle East). Health club industry revenue totalled US$14.4bn.

The IHRSA Asia-Pacific Health Club Report shows there is room for growth in the region, as the average member penetration rate is just 3.8 per cent. Australia and New Zealand lead with penetration rates of 14.8 and 11.4 per cent, respectively. Cities in Asia, including Beijing, Shanghai, Kuala Lumpur and Jakarta, are home to maturing industries, while future growth is anticipated in other expanding cities and in Asia-Pacific overall. Opportunities abound in the global economic powerhouses of China and India, with respective penetration rates of 0.4 and 0.12 per cent. Mainland China has around 2,700 health clubs with 3.9 million members, whereas India has around 3,800 health clubs and nearly one million members.

| |

|

Opportunities abound in the global economic powerhouse of China (above: Trainyard Gym, Beijing) |

|

|

|

|

| Originally published in HCM Handbook 2018 edition

|

|

|

|

|

| | |